I. Introduction

The sudden outbreak of the COVID-19 pandemic at the beginning of 2020 has had a negative impact on the global economy. As an important capital market of a country, the stock market can intuitively reflect residents’ financial behavior and a country’s economic conditions. Faced with COVID-19, firms have been impacted differently depending on their industry. To be specific, enterprises that are non-state-owned, engage in foreign trade or have few assets are more vulnerable to pandemics (Chen, 2020). Moreover, the pandemic contains risk transmission and risk spillover to other markets. Fang et al. (2020) analyze the influence of COVID-19 on the risk spillover of the money market, stock market, and other exchange markets based on an event study framework. They find that the COVID-19 pandemic had an immediate effect on various financial markets and the risk spillover of each market increases after 3-5 days of the event.

The literature on the COVID-19 pandemic is evolving (see Phan & Narayan, 2020; Sha & Sharma, 2020), and to-date studies have paid less attention to the consumer industry. The outbreak of the pandemic by restricting travel and movement of people has disrupted offline consumer purchases. It follows that even the basic consumption demands are difficult to guarantee. In this case, consumer pessimism may be transmitted to the stock market. Yu & Zhu (2015) find that investor sentiment has a notable negative impact on the stock price co-movement, indicating that the more pessimistic the consumer sentiment, the more intense the stock market’s response. On the other hand, Wang (2017) uncovers the inverse impact of Chinese stock price on consumer demand.

Employing an event-study approach, this paper examines the effect of the COVID-19 pandemic on the stock price movements of the consumer industry in China. The empirical results show that the COVID-19 pandemic had a huge impact on China’s consumer stock market in the short term. However, as the event unfolded, the return on consumer stocks gradually recovered. This finding implies that the impact of the pandemic on stocks of the consumer industry is limited and can be viewed as a conditional short-term phenomenon.

II. Methodology and Data

A. Methodology

The event study allows one to evaluate abnormal changes in sample stock prices (or index) following a specific event. Kothari & Warner (2007) provide an overview of the event study methods and conclude that short-horizon methods are quite reliable. Therefore, in this paper, we use an event study approach to examine the relationship between the COVID-19 pandemic and the abnormal returns in China’s stock market.

There are three models to estimate the normal rate of return, that is, the constant mean returns model, the market model, and the market adjustment model; see Kaketsis & Sarantis (2006). We find that intervention changes are assumed to be associated with the response of market rates in both the market model and the market adjustment model. Considering that the market rate of return is always changing and cannot be accurately determined by a fixed value, we use the constant mean return model to estimate the normal return rate, which is outlined as follows:

Riv=μi+ηiv(1)

σηiv=1V−1v∑v=1(Riv−μi)2(2)

Using the average index return, we can calculate the abnormal return :

ARit=Riv−μi(3)

Then, we calculate the cumulative abnormal rate of return for an event window is computed as:

CARj,T1,T2=T∑t=T1ARjt(4)

where, is the market return rate of the trading market, is the actual market return rate; is the variance of the sample in the estimation window, V is the length of the estimation window and v is any time in the event window. In this paper, and is the average index return rate over 140 trading days in the estimation window.

Based on the constant mean model, this paper examines the stock market’s reaction to the event in the event window and uses t tests to assess whether the outbreak of the event had implications for abnormal returns.

B. Data

On January 22, 2020 infected patients were identified and reported in 24 provinces of China. Meanwhile, the State Council Information Office held the first official conference on the pandemic on that day, which could be regarded as a signal that the pandemic in China had officially entered an outbreak state. Therefore, we choose January 22, 2020 as the event day of the COVID-19 outbreak. To improve the accuracy of the estimation as much as possible, we choose 140 trading days before the event date as the forecast period following Pan & Shi (2012). In order to capture the impact of major events on market expectations, it is necessary to examine event windows with different lengths. Therefore, this paper sets the event window for the outbreak of the pandemic as [-2, 2], [-5, 5], [-10, 10], [-15, 15] and [-30, 30].

The Shanghai Stock Exchange (SSE) Consumer 80 Index is used to measure the performance of stocks of the consumer industry. This index consists of 80 major consumers, optional consumer and medical & health companies in the Shanghai A-shares. The data are obtained from the RESSET Financial Database (http://www.resset.cn), which provides professional services for model testing, investment research, among others.

III. Empirical results

From Figure 1, we see the time trends of abnormal returns in consumer stocks. On the day that COVID-19 set in, the abnormal rate was unaffected. However, after the Spring Festival, the consumer stock experienced severe turbulence, which saw the abnormal return drop by 7%. In addition, although the abnormal rate had risen in the next few days, it is obvious that the stock market after the pandemic remained volatile, and the fluctuations were severe than before.

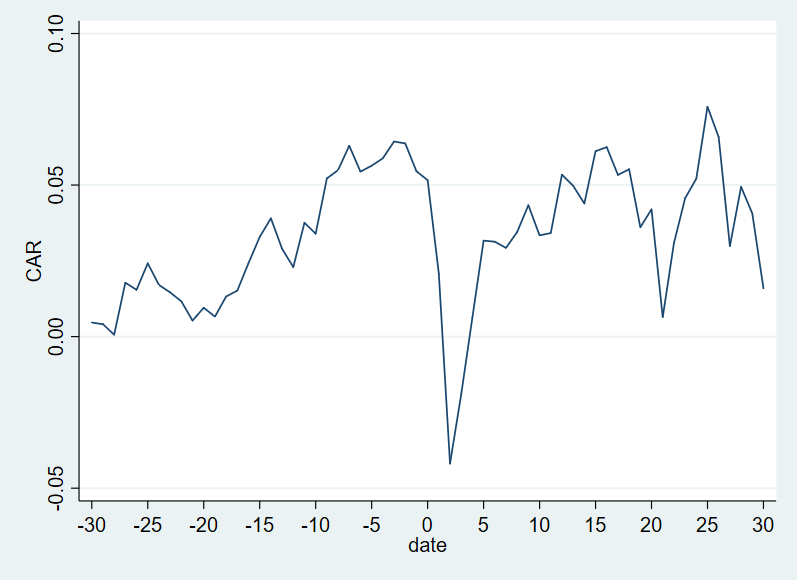

Figure 2 reports the time trends of the cumulative abnormal returns during the event windows. After the event day, we can see a sharp decline from 5% to -4%. Yet, on day 4, the CAR of the consumer industry started to rebound; it returned to positive values on the sixth event day and was in the 1% and 7% range from thereafter. This means that shocks like COVID-19 may produce a huge impact on the stock market within a short period of time, but as time passes and the event unfolds, its influence will gradually weaken.

The same conclusions can be obtained from the regression analysis. As shown in Table 1, the impact of COVID-19 is negative and statistically significant in the event windows of [-2, 2] and [-5, 5] at the 1% and 5% level, respectively. As the windows expanded, the negative impact of COVID-19 on the consumer industry falls in both significance level and magnitude. In the windows of [-10, 10], the effects of COVID-19 are not statistically significant. When the event window is expanded to [-15, 15], the impact of COVID-19 turns out to be positive at the 1% level of significance. However, this positive impact is transitory as we can observe that the significance disappears in the window of [-30, 30].

Some reasons may explain this phenomenon. As the stock prices fell, the Chinese government introduced a series of monetary policies to regulate the economy, which effectively helped to stabilize the stock market. In addition, the outbreak of the pandemic has positively influenced some industries, such as medical service, health, and information technology (He et al., 2020). Moreover, online shopping platforms and the mature logistics system in China also played an important role in boosting consumption during the pandemic.

IV. Conclusion

In this paper, we study the short-term impacts of the COVID-19 pandemic on stocks of the consumer industry in China. We employ an event study approach and use the Shanghai Stock Exchange 80 Index as the data sample. The empirical results show that the onset of COVID-19 had a significantly negative impact on consumer stocks at the very beginning of the crisis, especially on the second day after the crisis occurred. However, its negative impact does not last long. The consumer industry recovered quickly due to the government’s effective monetary policies and the well-developed online shopping industry in China.